By Nadia Elkaid, Noah Economidis and Anyssa del Castillo

Sam McCredie didn’t think twice about tapping his card for a $33.40 Uber Eats order, especially after applying a $10 discount. He expected to pay around $23.40.

“There was a delivery fee, and then a service fee. I didn’t even see it until it presented the total,” he said. “It felt like trickery.”

In the end, he was charged $28.90 — almost wiping out the discount entirely. “It kind of defeated the purpose of the $10 off,” he added.

The Uber Eats receipt. (Source: Samuel McCredie)

In a country where over 87 per cent of transactions are now digital, Australians are quietly paying hundreds of millions in card surcharges every year — often without knowing, and sometimes illegally.

A Central News investigation reveals how some businesses and online platforms are pushing, hiding, or inflating surcharges in ways that confuse consumers, undermine trust, and potentially breach national consumer laws.

Card payment origins

“What’s in your wallet?” asks actor Samuel L Jackson, the spokesperson for credit card company Capital One since 1994. The campaign, designed to promote the ease-of-use that credit cards offer, appealed to the growing American consumerism race that banks aimed to leverage.

In a time where cash was king, it was clear that banks worldwide were looking for new and inventive ways to increase consumer spending, and make it easier than ever to spend more.

Since that famous campaign, the world of monetary payments has changed. Credit card use has hit all time highs, and spawned a new era of fintech with the introduction of Apple Pay, Google Pay, PayPal and other online systems.

Now in 2025, it is easier than ever to use a credit card to pay for purchases, which has left cash use at an all time low. Consumers around the globe, especially in Australia, have turned to the convenience of tap to pay options in droves, with no sign of it slowing down.

This sentiment is echoed across the country. Cash is slowly dying in Australia, and the federal government is phasing out cheques by 2029.

Even big supermarkets like Woolworths have toyed with the idea of card-only stores that feature no cash checkouts, due to the small volume of transactions cash accounts for.

Surcharging rise

But an unfortunate trend has followed. Since its introduction, transaction fees and surcharges have led the way in adding small indexes onto the majority of purchases.

Whether it’s buying a coffee or a new computer, card transactions often cost more than cash ones, largely due to the infrastructure required for payment machines and terminals.

Every time Australians tap their card, banks and payment networks charge merchants up to 2 per cent — and many businesses pass that cost straight back to customers.

According to Reserve Bank data, Australians now pay nearly $960 million a year in card surcharges, often without realising until after they have tapped.

Morgan Campbell, Head of Policy at CHOICE, says the problem is twofold: “The additional cost surcharges put on top of what we’re already paying, and the lack of transparency about how that cost is arrived at.”

Most Australians don’t discover the fee, or the reason for it, until they’re about to tap.

Payment platforms like Visa, Mastercard and PayPal argue surcharges are necessary to cover the high cost of running secure, reliable systems.

They say these fees fund fraud protection, transaction processing, and technology infrastructure — all of which make card payments fast and convenient for both consumers and merchants.

Struggling small businesses

The biggest concern comes from small businesses. In order to have simple card terminals, Australian businesses have to pay high fees to allow for convenience for its customers.

While the cost is high, Australia’s increasingly digital and tap-to-pay transactions have made it near impossible for any business to not accept card payments.

That shift means card machines — Eftpos terminals, Square readers and similar devices — are now standard in restaurants, cafés and bricks-and-mortar shops across Australia. Every one of those businesses pays a fee to use the service.

At La Herradura Coffee Stable in Chippendale, co-owner Santiago Quintero says its card surcharge is clearly displayed at checkout, yet confusion still occurs “at least once a week”. Customers often question why their total is higher than expected, or assume the café is pocketing the extra charge.

“We charge what the machine tells us,” he explains. “But even I don’t fully know what Square or Smartpay is charging — they say it’s a 1.6 per cent flat rate, but sometimes more is taken out.”

After a year, La Herradura switched providers upon realising its old bank terminal was cutting into already thin margins.

“At some point, we were paying out of pocket,” Quintero says. “Now we pass the cost on, but we don’t make a cent from it.”

He believes card payment processors and banks should be more transparent with both merchants and customers. “Most people don’t even know their debit cards are being surcharged,” he says. “They just tap and go.”

If debit card surcharges are banned, Quintero says the café would likely be forced to raise prices. “We’d have no choice — the fees are real, and the profit margins are small,” he adds.

Small business response

Source: Reserve Bank Australia

Industry body AusPayNet says the confusion Quintero describes is widespread. In its submission to the RBA, the network admits “the complexity of current scheme fee structures … presents a challenge for both industry participants and stakeholders,” adding that even large payment-service providers struggle to decode their own fee schedules.

That complexity trickles down to cafés like La Herradura, whose owners must explain a surcharge they themselves only partially understand — and whose customers then blame the venue, not the opaque system behind it.

That lack of transparency doesn’t just frustrate businesses. Campbell says the system has become “so complex and so opaque that most of the time, consumers haven’t got a clue if the surcharge they’re paying is a fair response to the business’s cost, or just a sneaky way to up the price”.

Balmain retailer James Keremelevski tells the same story from the other side of Sydney.

“Nine out of 10 purchases are card-only,” he says. “We run both an EFTPOS bank terminal and Square, and people just tap without thinking.”

The fee, however, is anything but automatic: Square clips a flat 1.6 per cent on every tap, while the bank terminal varies by card type.

Keremelevski usually passes that charge on. “It depends on the transaction — sometimes it’s just a few cents, other times it’s more than a dollar, and that usually gets passed onto the customer,” he says, adding that absorbing the fee “would wipe out the margin on small items”. Even processing a refund costs him.

“It’s about $10 in EFTPOS fees just to give a customer their money back, and we can’t pass that on, so we wear it,” he says.

Two different businesses, two different terminals, but the same outcome: customers blame the shop, while the real cost of tapping is buried in a thicket of back-end charges.

Consumer perspective

Central News ran a survey of 30 people to see gauge how widespread the confusion is. Nearly nine in 10 (87 per cent) said they’d been hit with a surcharge in the past month, and almost two thirds (63 per cent) only noticed after they had already tapped.

While 97 per cent believed businesses should display the exact fee before payment, the same proportion said signage is “somewhat clear” at best — or not clear at all.

Almost half (47 per cent) said they felt outright misled when a surcharge isn’t disclosed and 70 per cent had switched to cash or another payment method to dodge the extra cost.

A full 60 per cent believed card surcharges should be scrapped entirely. Even in 2025, a lack of transparency remains the norm and it’s driving consumers to change how they pay.

Source: UTS Survey

Are banks acting in their own interests?

Banks may not profit directly from the surcharges consumers see on receipts — but they do benefit from the system that enables them.

According to Former NAB lending specialist Enes Mohammad, surcharges typically go to the business, not the bank. But every card transaction still generates merchant service fees, which include interchange fees, scheme fees, and provider margins — all revenue streams in which banks have a stake.

“The surcharge itself isn’t bank revenue,” Mohammad explains. “But the transaction enabling it is.”

And it’s a system that favours scale. Large corporations process massive volumes of payments and have the leverage to negotiate lower fees. Small businesses, meanwhile, are often locked into bundled pricing plans with higher rates, higher risk profiles, and limited ability to shop around.

“The system’s not necessarily designed to be unfair,” Mohammad says, “but it’s definitely structurally imbalanced.”

As for responsibility? Mohammad says banks do provide merchants with disclosure documents and onboarding materials, but they don’t monitor surcharge compliance — especially when third-party terminals like Square are involved.

“Compliance is largely left to the business,” he says, “unless challenged by regulators or customers.”

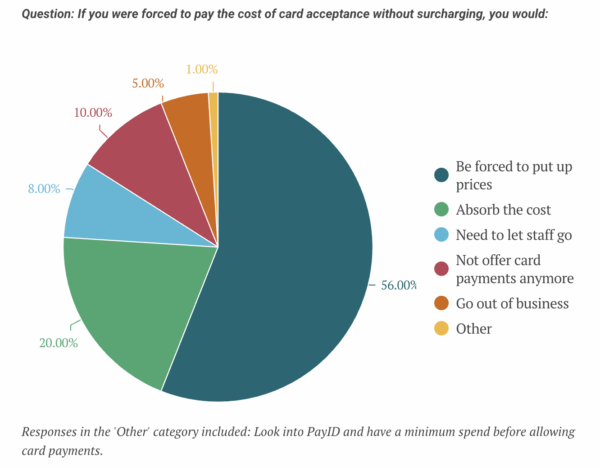

Mohammad acknowledges that while a ban on surcharges may seem fair to consumers, it could place further pressure on small operators.

“Surcharges are often crucial to offset processing costs. If they’re removed, many businesses may just raise base prices instead — or shift toward lower-cost options like PayID or EFTPOS.

Source: UTS Survey

The surcharge ban

Ahead of the 2025 election, Prime Minister Anthony Albanese argued that card surcharges were outdated in an era of modern payment technology, and discussed a reduction in overall small-business payment fees.

Labor’s proposal would effectively abolish card surcharges, requiring all card payments to match the recommended retail price displayed at checkout.

In theory, the plan could save consumers nearly $1 billion a year — a move aimed at easing cost of living pressures.

But not everyone is convinced. Australia’s big banks warn that a complete reduction in surcharge payments could have unintended consequences, especially for small businesses, which may need to raise prices to cover the costs.

Whilst the ACCC’s 2017 rule requires surcharges to reflect only the “cost of acceptance”, the federal government’s proposal would simply eliminate them altogether.

Banks warn this could lead to higher retail prices and strain payment infrastructure. Both NAB and ANZ have expressed reservations and have called for a review into surcharging practices, particularly around buy now, pay later services.

The proposal, which would see card surcharges scrapped by January 2026, is reliant on RBA approval and support from both small businesses and major banks.

Financial advisors warn that if the proposal were to go through, businesses may need to raise their prices to absorb the cost of card fees — a burden many can’t afford to carry.

Insiders warn this could potentially lead to a larger downturn in consumer spending and add further pressure to already rising living costs.

Wes Lambert told the Seniors Discount Club that “the potential surcharge ban is actually going to turn into an inflationary pressure for menu prices,” as restaurants and café’s would be forced to raise the cost of goods.

Consumer advocates see it differently. Campbell argues a debit-card surcharge ban would “absolutely benefit customers. Some businesses will simply drop the extra charge; others might fold it into the upfront price. Either way consumers win — they pay less, or they know the full cost before they buy.”

A small-business lobby group, the Independent Payments Forum Australia, told the RBA that banning surcharges now would unfairly penalise cafés and corner stores, which still pay higher card fees than major retailers.

The forum supported stronger regulation but warned that “a ban should wait until small businesses are on a level playing field — and until existing laws are actually enforced.”

Yet even under today’s current rules, enforcing surcharge compliance is far from simple.

In its submission to the RBA, AusPayNet warned that the system’s complexity leaves “smaller merchants responsible for updating the surcharge rates for different card types … [and] the frequent changes required can lead to input errors, confusion about the correct rates to apply, and simple administrative procrastination or forgetfulness.”

In other words, while a ban might simplify things for consumers, it won’t resolve the paperwork maze businesses and regulators are already navigating.

Increasing world of fees

Card surcharges don’t just stop at the checkout counter. Online retailers have been caught inflating prices through hidden transaction fees – often revealed only at the final stage of purchase.

Food delivery apps such as Uber Eats and DoorDash have faced criticism for this tactic which keeps fees out of sight until the end of the checkout process. This practice — known as drip pricing — starts with a low upfront price, then adds charges — like service and delivery fees — step by step as the customer proceeds. The real total only appears on the final screen.

Behavioural economists say drip pricing exploits the sunk-cost fallacy: once shoppers have invested time building an order, they’re reluctant to abandon it, even if the final price is much higher than expected.

Ticketing platforms Ticketek and Ticketmaster have also come under scrutiny for similar practices, layering “handling” and “payment processing” fees that push the final total well above the advertised fare.

These additional charges help ticketing duopolies rake in billions in extra revenue and fuel increasingly aggressive pricing models. In some cases, these have included surge pricing, which adjusts ticket prices based on demand.

Both companies have faced backlash and were even called to testify before the US Congress to defend their practices, amid accusations of anti-consumer behaviour.

Holidays and surcharges

Surcharges can also vary by day. Under the Hospitality Award, cafés must pay staff 25 per cent extra on Saturdays and 50 per cent on Sundays and public holidays, costs many venues recoup through weekend or holiday surcharges.

According to the ACCC, these fees must be “clearly visible before the customer orders,” either on the menu or on signage.

On public holidays, these charges can reach up to 17 per cent of the total bill, adding extra pressure on consumers at the checkout.

La Herradura also applies a weekend and public holiday surcharge, which Quintero says is clearly displayed — but confusions still happen.

“Sometimes people say, ‘Why is it more expensive today?’ and they think it’s the card fee again,” he explains.

In reality, the weekend surcharge covers staff penalty rates, not payment processing. “We pay 50 per cent extra in wages on weekends,” he says, “and then on top of that, the card provider still takes their 1.6 per cent.”

Even with signage, he says the overlap between different fees creates confusion — especially when customers don’t understand who the charges actually go to.

Global comparison

It’s not just here at home that fees and surcharges have taken hold. Around the world, additional fees are on the rise — especially post-COVID-19 and the boom in online shopping. The United States has been hit particularly hard.

The US Supreme Court decided to take matters into its own hands, hearing a case on whether state bans on credit card surcharges should be allowed. However, the Justices ended up being split on the issue — conservative judges were concerned about the application of the bans, while liberals were worried it could violate retailer’s free speech rights.

The law was argued to be unconstitutional, on the grounds that it restricted retailers’ free speech rights. It allowed businesses to offer a cash discount, but not to explicitly add a surcharge for card payments.

Australia has clearly not followed suit to the same standard as the US. While the Albanese Government aims to outlaw surcharges, both the Reserve Bank of Australia and the Australian Competition and Consumer Commission still reserve the right to approve or deny the federal government’s plan, which could spell trouble for a potential surcharge ban.

In contrast to overseas banks, Australian institutions remain far more cautious. While US organisations like Capital One and Bank of America have shown support for eliminating surcharges, Australian banks have been much more reluctant to support the current proposals.

This resistance could create further challenges for the federal government if it continues to push for a nationwide surcharge ban in the coming fiscal year.

Surcharges were designed to recover costs. Somewhere along the line, they became something else — hidden, habitual, and hard to trace.

Whether it’s a coffee, a concert ticket, or a burger delivered to your door, the price you still see often isn’t the price you pay. And while politicians debate bans and banks debate risk, consumers keep tapping and guessing.

Main image by Project 365 in a day/Flickr.