*(Photo: Pat Fordham)

Patrick Fordham from the University of Technology Sydney (UTS) and Antonia Fieldhouse from The University of Huddersfield UK, search for the road to economic recovery after COVID-19.

Economists and academics are warning that governments need to do more to ensure that any post-pandemic recovery is swift.

Professor of Economics at the University of Canberra Dr John Hawkins, says the Morrison Government’s decision to make JobKeeper a two-tiered system from September 28, leaves the economy vulnerable.

“I don’t think the economy will be anywhere near recovered by September, so I think that higher payment should keep going,” he said.

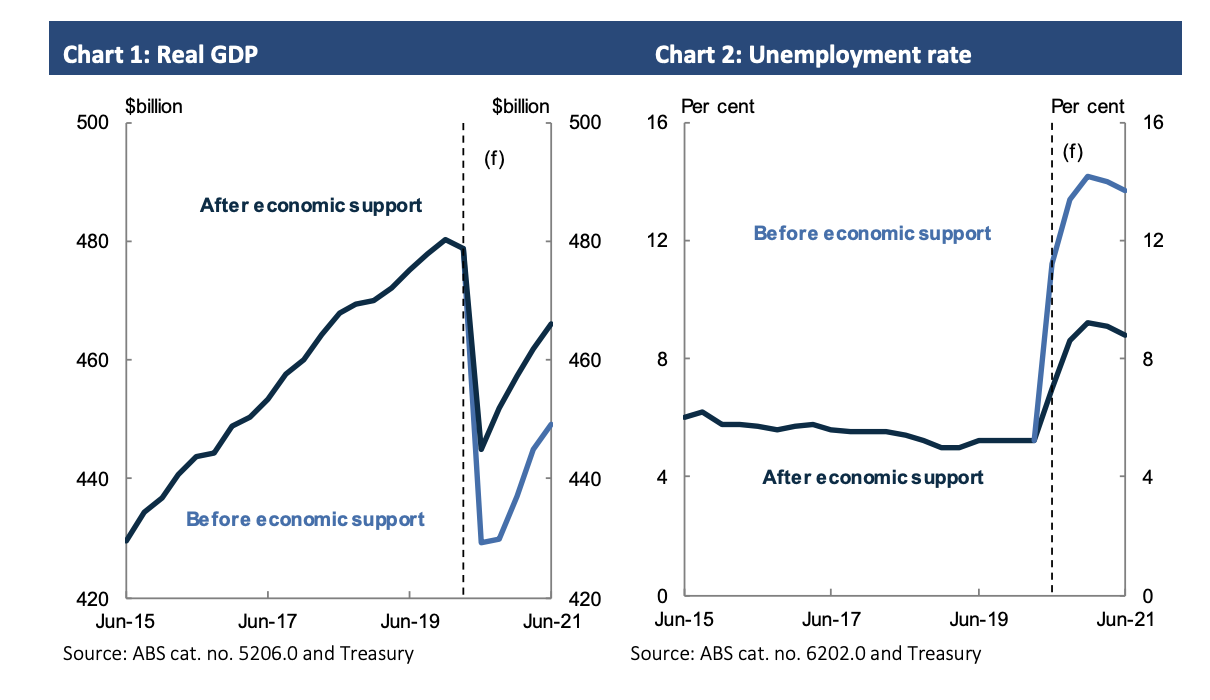

Australia has suffered one of its largest economic downturns in recent history with Federal Treasurer Josh Frydenberg revealing the nation’s debt hit $86 billion last financial year. It’s the biggest budget deficit since the Second World War and has plunged the economy into recession for the first time in 29 years.

Given the Treasurer’s bleak assessment, Professor Hawkins believes that economic recovery will not come anytime soon. “September looks to be better but won’t offset all of the fall in June.”

Screenshot (Source: Australian Bureau of Statistics)

In the June quarter, the country’s GDP fell by 0.3 per cent, prompting the Treasurer’s announcement that the country was in recession for the first time in 29 years.

However, Professor Hawkins says the debt impacts of COVID-19 have been lessened by years of strong economic management.

Reserve Bank of Australia, Sydney (Photo: Pat Fordham)

“A reason why it’s not so much of an issue, is that interest rates and government debt are so low at the moment. A three-year government bond yields around a quarter of a per cent and a 10-year yield is under 1 per cent, so the interest burden of that debt is much smaller than it would’ve been compared to historical norms.”

The country’s strong economic standing before COVID-19 is why the government could provide more relief to Australians, according to Professor Richard Holden from the University of New South Wales (UNSW).

“The cost of borrowing is incredibly low, so I think there [is] certainly an option to do more. We came into this situation with one of the lowest debt-to-GDP ratios in the world, so we certainly have the capacity to do that,” he said.

As an example, Professor Holden argues that Treasurer Frydenberg should take the UK Government’s lead in its wage subsidy programme.

“Something closer to the UK’s scheme – while many other countries had this as well – of wage replacement up to 80-90 per cent – up to a fairly generous cap.”

In its latest estimate released on June 12, the UK Office for National Statistics (ONS) reported that the country’s GDP fell by 10.4 per cent% in the three months to April 2020, which Deputy National Statistician for Economic Statistics Jonathan Athow, described in a media release as a “historical fall”.

Barclays Bank, Huddersfield, UK (Photo: Antonia Fieldhouse)

“April’s fall in GDP is the biggest the UK has ever seen, more than three times larger than last month and almost ten times larger than the steepest pre-Covid-19 fall,” he said. “In April the economy was around 25 per cent smaller than in February.”

According to the ONS, an estimated 12.5 million people have reported a reduced income as a result of the virus, with people on lower personal incomes working fewer hours and being less able to save for the future.

Jo Michell is an Associate Professor in Economics at the University of the West, Bristol (UWE). He also described government support for these lower income earners and renters as essential in the current economic climate.

“[We need] some return to economic activity, with continued financial support for those unable to return to work,” he said.

This is echoed by University of Leeds Professor Marco Veronese Passarella, who points to possible solutions such as continued support for low income workers and structural reform.

“[Economic recovery] is feasible as long as the government can support [low income workers] until the crisis is over,” he said.

“A different model of development [could include] less predatory finance, less polluting activities, and more sustainable manufacturing.”

Pat Fordham @PatFordhamnews and Antonia Fieldhouse